US equity futures lower; Brent continues to slide with focus on ships traversing the Strait - Newsquawk US Market Open

- Iranian Deputy Foreign Minister said the safe passage through the Strait of Hormuz without consideration of Iran's sovereignty is not guaranteed. This follows an Iranian strike on a Singapore-flagged cargo ship after failing to follow the set route.

- US President Trump said we have a new market coming up called Iran and added that Iran wants to make a deal with us very badly and thinks they will make a deal.

- US equity futures are softer, with the NQ underperforming after further tech selloff in South Korea.

- DXY continues to pull back but remains firmly above the 100.00 handle; G10s are broadly firmer with the EUR outperforming.

- Fixed income benchmarks are off best levels as the haven bid returns to bonds.

- Energy benchmarks continue to fall despite the recent strike on the Singapore cargo ship.

- Looking ahead, highlights include US Goods Trade Balance Advance (May), Wholesale Inventories (May), UoM Sentiment Final (Jun), Speakers including Kashkari, ECB's Vujcic, RBNZ's Bremen and Norges Bank's Bache.

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

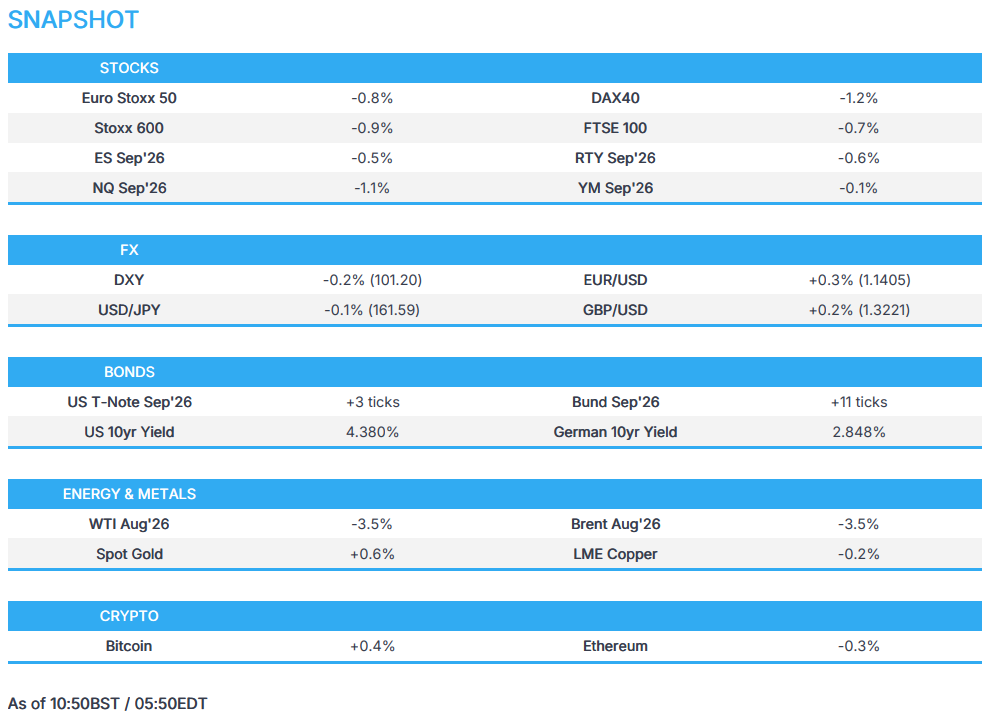

- European bourses (STOXX 600 -0.9%) are entirely in the red in the last session of the week, driven by another day of losses in South Korea (SK Hynix -8.4%, Samsung -5.3%). Some analysts are citing Apple's price hikes on products due to memory chip shortages as a catalyst for the recent sell-off, raising concerns that rising component costs could curb demand for devices. An analyst at Javelin Wealth Management also said the recent gains for chipmakers could come at the expense of product manufacturers. The losses in South Korean giants have weighed on European chip names (Infineon -3.1%, ASML -1.0%) and indices composed of technology companies (DAX 40 -0.8%, AEX -0.6%).

- European sectors highlight a negative bias. Optimised Personal Care (+0.8%), Food, Beverages & Tobacco (+0.6%) and Utilities top the sector pile. Energy (-1.5%) is the underperformer again, with Technology (-1.4%) and Financial Services (-1.1%) also lagging.

- US equity futures are mixed, with the NQ (-0.9%) holding onto Thursday's sell-off, though off its worst levels. After-hours, ON Semi (-10% pre-market) announced the acquisition of Synaptics (+7.6% pre-market), totalling c. USD 7bln.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- USD finds itself under modest pressure. DXY at a 101.18 base, but well clear of the 100.76 WTD low, with the index set to see the week out around the middle of its range. In brief, a tale of two halves for the index which began the week on the front foot before reversing after Thursday’s data deluge and continuing to slip since.

- EUR outperforms as a result of the continued USD pressure. No real move to the ECB CES, which showed a moderation in the 12-month price view and an uptick in the growth view. The growth revision is not enough to provide comfortable space for further tightening, and equally the price moderation is not sufficient to take another move off the table. Nonetheless, the price moderation does add to the post-PMI & Lagarde dovish tilt we have seen in recent days.

- In more detail, EUR/USD has breached 1.14 to the upside. Picking up gradually across the morning, as the US data on Thursday has and continues to permit an unwinding of some of the yield differential moves we have seen in recent days, with the Fed more-hawkish and ECB mixed but net less-hawkish, particularly from Lagarde as referenced. However, while it has hit a 1.1407 peak, EUR remains in the red on the week and continuing the near unbroken downward trend of the last seven weeks.

- Elsewhere, G10s generally are slightly firmer against the USD. With GBP the next-best behind EUR, comfortably above 1.3200 and flat/firmer WTD, but again, still towards post June policy announcement lows, as BoE expectations coalesce around the on hold for the foreseeable narrative, despite the hawkish dissenters.

- CAD, JPY and CHF all faring around equally. Of those, USD/JPY participants remain on watch for potential intervention risk, particularly as Japanese authorities tend to target Friday’s and go with the market move rather than fighting it. USD/JPY just above a 161.53 base, and while the JPY is firmer today the bearish trend remains near-enough unbroken at a weekly level over the last month and a half.

- Today is spot month/quarter-end. As a reminder, Barclays model was neutral overall for the USD against all majors, formed of a moderate USD buying signal on the month-end, but countered by a strong USD sell signal for quarter-end.

FIXED INCOME

- Global fixed benchmarks are firmer across the board as government debt returns as a place of safety, with tech stocks weighing on the broader equity space. Energy prices also continue to fall, which further drives the fixed-income space higher.

- Bunds (+12 ticks) have extended on Thursday's high to make a new WTD high, currently trading at the upper end of the 127.25-127.64 range. The ECB released its May Consumer Expectations Survey, in which it showed consumers expect inflation to fall to 3.5% next year, down from April's 4% figure. This comes as a surprise, as the survey was conducted before the signing of the US-Iran MoU. Despite this, the German benchmark was unreactive. In terms of market pricing, the ECB is still expected to hike once more by year-end, with only a 12% chance of two more hikes.

- USTs (+4 ticks) are bid, trading towards the upper end of their 110-00+ to 110-09+ band, with the 10yr yield touching 4.37%. The MOVE index has completely reversed the wartime bid seen at the start of the Iran war, and with BofA's weekly flow report showing USD 16.6bln of flows into bonds, it potentially shows a renewed demand for debt. Looking ahead, a lack of tier 1 data, with final University of Michigan figures ahead, while Fed's Kashkari is also expected to be on the wires.

- Gilts (U/C) remain on high alert for any updates on who the newly-appointed MP (and expected PM) Burnham will choose for Chancellor, with Reeves not expected to stay in the role. More recently, The Times's Swinford reported that it will more likely be a two-horse race between Ed Miliband and Shabana Mahmood, with people close to Streeting stating that they do not think he will get the job. The fact that Miliband is still in the running could put a ceiling on gilts.

- Italy sells EUR 7bln vs exp. EUR 5.5-7bln 3.15% 2031, 3.80% 2036 and 3.45% 2036 BTP & EUR 2.0bln vs exp. EUR 1.5-2bln 1.645% 2036 CCTeu.

COMMODITIES

- The US-Iran situation remains complex. It was reported that the IRGC attacked a Singapore-flagged cargo ship, after it attempted to traverse through the Strait through a route not designated by the Iranians. This led the UN to pause its evacuation plans for ships around the Strait. Despite the attack, Bloomberg data continues to indicate that ships continue to traverse through the Hormuz, highlighting that traffic continues to flow in “both directions”.

- On the Lebanon front. The US-mediated Lebanon-Israel talks were expected to conclude on Wednesday, but were then extended into today. Israeli sources have suggested that there has been some progress, but no deal has been reached thus far. The negotiations focus on the withdrawal of Israeli troops from southern Lebanon; there may be a chance that Israel will only withdraw from areas where operations have already been concluded, and continue such action in other parts of the region. Therefore, the risk is that Iran is not satisfied by the outcome of the talks, and potentially restart closures of the Strait.

- Crude benchmarks are in the red, with WTI (-3.5%) and Brent (-3.4%) holding at the bottom end of their respective USD 68.98-71.86/bbl and USD 72.14-75.13/bbl ranges. Despite the flare-up on the Strait in the prior session and the continued lack of progress between Lebanon and Israel, crude prices continue to slip. It is the case that as long as ships continue to traverse the Strait, other friction points can be ignored… at least in the short term.

- Spot gold (+0.2%) is ever so slightly firmer this morning, but continues to remain near recent troughs. Today, the yellow-metal holds just above the USD 4k/oz mark, and within a USD 3,982-4,039/oz range. Elsewhere, base metals are broadly slightly lower this morning, with 3M LME copper currently off by c. 0.6%. It currently holds around USD 13.25k/t and within a USD 13,088.3-13,281/t range.

- Saudi Aramco reopened the Ras Tanura oil loading operations after a prolonged halt, with two supertankers loading oil at Ras Tanura on Friday, while another is awaiting loading, according to shipping data.

- Several Japanese-related vessels passed through the Strait of Hormuz as part of IMO evacuation plans, which have since been suspended following the attack on a cargo ship, according to Mainichi.

- China's MOFCOM released a list of non-state Chinese companies eligible for oil imports.

- Kazakhstan cut the gas production at the Karachaganak gas field after Ukraine drone attacks on Russia's Orenburg gas processing plant. Raw gas from the field is usually delivered to the Orenburg plant.

- Kazakhstan Energy Minister said we may consider fuel exports to Russia if there is an official request.

- Russia is considering a short-term ban on diesel exports for a few months, TASS reported.

TRADE/TARIFFS

- US Commerce Department banned sales of Geely (175 HK)-owned Chinese luxury EV Polestar, from 2027 onwards.

NOTABLE EUROPEAN HEADLINES

- The Times' Swinford reported that it is likely to be a two-horse race between Ed Miliband and Shabana Mahmood for chancellor, with allies of Streeting say they do not think he will get the job.

NOTABLE EUROPEAN DATA RECAP

- ECB Consumer Expectations Survey (May): 1-year inflation expectation 3.5% (prev. 4.0%), 3-year inflation expectation 2.9% (prev. 2.9%), 5-year inflation expectation 2.4% (prev. 2.4%), 1-year Economic growth expectations -1.7% (prev. -2.2%).

- Italian Consumer Confidence (Jun) 92.4 (Prev. 93.4).

- Swedish PPI MoM (May) M/M 1.3% (Prev. 1.1%).

- Swedish Consumer Confidence (Jun) 93.6 (Prev. 92.4).

CENTRAL BANKS

- Fed's Goolsbee (2027 voter) said it is difficult to determine whether inflation pressures are persistent or temporary, while noting inflation is moving in the wrong direction, and some of that is being driven by one-off factors. He added that inflation remains more concerning on the services side and that spending based on expected future gains makes him concerned about potential inflationary pressures. Goolsbee also said there are some signs of improvement in services inflation, but it remains well above where it needs to be, as well as stated that core inflation it is still too high and trending in the wrong direction, while services-driven core CPI is more concerning than inflation driven by goods or oil-related items. Furthermore, he stated that wages are not a particularly good leading indicator for inflation and that inflation could rise before wages do, adding that inflation needs to be monitored closely.

NOTABLE US HEADLINES

- US President Trump's administration asked OpenAI to restrict the launch of its next model, GPT-5.6, to only a small set of government-approved partners before a wider release due to security concerns, according to a source cited by Axios.

- Representatives Gottheimer (D) and Moolenaar (R) are reportedly introducing legislation that would allow US cloud companies to report suspected foreign misuse of advanced AI computing, Axios reported.

- BofA's weekly flow report notes USD 25.5bln out of cash, USD 5.0bln out of stocks, USD 16.6bln into bonds, USD 0.5bln out of gold. Bull & Bear Indicator fell to 9.1 (prev. 9.2)

GEOPOLITICS

MIDDLE EAST

- US President Trump said they have a new market coming up called Iran, and that Iran wants to make a deal with them very badly, while he thinks that they will make a deal and stated the Strait is open.

- Iranian Deputy Foreign Minister said safe passage through the Strait of Hormuz without consideration of Iran's sovereignty is not guaranteed and that any framework for passage through Hormuz must be in coordination with Iran, otherwise it will be suspended from the designated route.

- N12's Segal posted after a conversation with a source on the Iranian issue, "His opinion on the agreement and the situation is much less negative than what has been written anywhere else, including here."

- Iran's Khatam al-Anbiya Central Headquarters declared that if the US is unable to contain and control the Zionist regime, Iran will not tolerate any threat against itself and considers it its right to respond to these dangerous actions.

- Israeli Embassy in Washington said due to extension in the discussions, negotiations between Israel and Lebanon mediated by the US will continue on Friday for a fourth day, according to a Kan reporter.

- Israeli Energy Minister said the withdrawal from southern Lebanon is not under consideration and would be rejected even if requested by US President Trump, while he stated that Israel does not plan to occupy all of Lebanon, but intends to establish full security control over the entire Gaza Strip.

- Israeli PM Netanyahu said that we will remain in the security zone in southern Lebanon as long as necessary and have ordered the army to have complete freedom of action to counter any threat against our forces or residents of the North.

- UN said the Lebanon ceasefire is largely holding, though Israeli military operations inside Lebanon continue. It was separately reported that Israel's military conducted airstrikes on Beit Yahun, Lebanon, while Israeli tank movements were reported in Wadi Saluqi and Bint Jbeil, Lebanon.

- IAEA chief Grossi said it's undeniable we have an agreement that IAEA will have access to Iran for inspection, while added that they hope to resume their work in Iran soon.

- GCC Secretary General said the proposed USD 300bln for the reconstruction of Iran has not been presented to us officially or unofficially, and it has not been discussed with the US, Sky News Arabia reported.

RUSSIA-UKRAINE

- Russia claimed to have shut down 660 Ukrainian drones overnight, Moscow's mayor reported that 47 drones were intercepted that were heading to the capital.

OTHER

- North Korean leader Kim oversaw the testing of key weapons, according to KCNA.

CRYPTO

- Bitcoin has returned to the USD 60k handle, rebounding from 3 straight days of selling. There was minimal reaction after Strategy's CEO reaffirmed the Co.'s focus on the crypto coin.

APAC TRADE

- APAC stocks were pressured following the choppy performance stateside, where markets were indecisive amid two-way trade in tech, a recent data deluge and a rebound in oil. The overnight deterioration in risk sentiment coincided with renewed selling in tech after Apple raised prices of some products by nearly 20% and with OpenAI leaning towards delaying its IPO until next year.

- ASX 200 was rangebound with the index cushioned as the underperformance in tech, telecoms and healthcare was partially offset by resilience in some defensive stocks.

- Nikkei 225 suffered heavy losses as tech stocks dominated the list of worst performers, with SoftBank down by a double-digit percentage owing to its large exposure to AI and semiconductors.

- KOSPI remained volatile with the slump triggering a sidecar and eventual circuit breaker alongside notable declines in both Samsung Electronics and SK Hynix.

- Hang Seng and Shanghai Comp conformed to the sell-off across the region amid the tech rout.

NOTABLE ASIA-PAC HEADLINES

- China sharpened tools for retaliating against foreign sanctions with Beijing preparing a new law that would add to its ability to punish foreign companies and individuals deemed to harm Chinese interests, according to WSJ.

- PBoC has requested that some commercial banks increase lending in June amid ongoing weak credit demand, according to reports.

NOTABLE APAC DATA RECAP

- Japanese Tokyo CPI YY (Jun) 1.7% vs. Exp. 1.7% (Prev. 1.4%).

- Japanese Tokyo CPI Ex. Fresh Food YY (Jun) 1.6% vs. Exp. 1.6% (Prev. 1.3%).

- Japanese Tokyo CPI Ex Food and Energy YY (Jun) 1.9% vs. Exp. 1.8% (Prev. 1.6%).

Badenoch blasts 'moaning' female Labour MPs over Burnham jobs 'quota'

Kemi Badenoch has told Labour women to earn a job in Andy Burnham's Cabinet instead of demanding they are handed jobs because of their gender.

The Tory leader lashed out today amid reports that female MPs are demanding the de-facto new prime minister introduce a 50:50 gender split 'quota' in his government.

Amid reports that former foreign secretary David Miliband is being lined up to return to the role, possibly with his brother Ed as Chancellor, one female minister also complained that Burnham could not have 'more Milibands than women' in the top posts.

But in a scathing article in the Times today Mrs Badenoch told them to 'stop moaning' and get chosen on merit instead of retreating into 'more of the failed identity politics that is holding back our country'.

'There are many, many reasons why you shouldn't have any Milibands in the cabinet,' she said.

'But complaining that the boys haven't given them the right jobs or that the boys are taking all the jobs, just shows that Labour's women still don't get it.'

The idea of quotas was also attacked by Baroness Jacqui Smith, Labour's Skills Minister.

Asked by Times Radio if Mr Burnham should reserve jobs for women, she said: 'No, I think what Andy Burnham should be doing is building the very best team around him to change this country.'

A letter written by the Women's Parliamentary Labour Party has called on Mr Burnham to ensure a 50:50 split between men and women in government jobs

Amid reports that former foreign secretary David Miliband (above, right, in 2010) is being lined up to return to the role, possibly with his brother Ed as Chancellor, one female minister complained that Burnham could not have 'more Milibands than women' in the top posts

But Mrs Badenoch told them to pipe down and get chosen on merit instead of retreating into 'more of the failed identity politics that is holding back our country'

A letter written by the Women's Parliamentary Labour Party and seen by the BBC has called on Mr Burnham to ensure a 50:50 split between men and women in government jobs after he succeeds Sir Keir Starmer.

'We are asking you to demonstrate this change from day one and address the toxicity and misogyny within our own party and government,' it said.

Labour has never had a female leader, while the Conservatives have had three, and Mrs Badenoch urged the government to follow its meritocratic example.

'If you run a meritocracy, then you do not have to worry about jobs for the boys,' she wrote.

'Every woman who is a Conservative MP, every woman who has ever won the leadership, has had to fight to get where she is.

'By contrast, Labour women are demanding guarantees from Burnham. But the truth is he doesn't have to give any guarantees.

'If none of Labour's women are prepared to get their hands dirty and challenge him for the leadership, their demands are toothless.'

'In fact, it's quite revealing that the women's parliamentary Labour Party has written to Burnham asking him to commit himself to at least 50 per cent female ministers.

'This has nothing to do with meritocracy. It is yet more of the failed identity politics that is holding back our country.'

Venezuela Fury and Noah Price subsidising their life by livestreaming

Venezuela Fury and her husband Noah Price look to be making their own way in the world by raking it in from their lucrative social media accounts.

The influencer daughter of Tyson and Paris Fury, 16, has become an internet sensation after tying the knot with her husband Noah, 19, earlier this year.

Since getting married and moving in together the couple have been earning thousands of pounds a month, livestreaming their life as newlyweds in their static caravan in the East Riding of Yorkshire.

And fans can't get enough of their regular life updates on TikTok and Kick, which have proved to be very profitable for the pair.

They look to be supporting themselves after Noah denied that he was given £5million by Venezuela's family as a wedding gift.

Despite his wife's huge family wealth, an estimated combined £160 million, Noah recently told his Kick followers that he 'pays for everything' for the couple.

Making light of the claims about Venezuela's millionaire financial status, Noah said: 'I actually pay for everything unfortunately. You'd expect the millionaire to pay for it wouldn't you.'

Venezuela Fury and Noah Price are earning thousands livestreaming their caravan life - after her new groom insisted he pays all the bills and denied he had £5m handout from her dad

The influencer daughter of Tyson and Paris Fury , 16, has become an internet sensation after tying the knot with her husband Noah, 19, earlier this year

Venezuela then asked their fans: 'Do you think I am a millionaire?'

Noah joked: 'She isn't a secret millionaire guys', before she broke into song and sang: 'But I live like a millionaire!'

But it seems according to estimated calculations from their social media work, Noah and Venezuela can more than afford to support themselves.

Noah has been livestreaming on platforms such as Kick and TikTok, where viewers can send paid gifts or donations.

He was previously encouraging viewers to send gifts on his honeymoon during livestreams, suggesting this is one revenue stream.

Both Noah and Venezuela have built substantial followings on Instagram and TikTok. They can potentially earn money through sponsored posts, brand collaborations, affiliate links and creator payouts.

Kick allows its creators to take home 95 per cent of the £4.99 subscription cost that fans pay.

Streamers keep 100 per cent of direct tips and donations, minus minor standard payment processing fees.

It is unclear how many subscribers Noah currently has because this information is hidden, but he does have 7,200 followers which is publicly viewable.

An industry insider has suggested Noah is making around £400 per video on TikTok, while Venezuela is likely to make £2,000 due to her following count of 1.3 million.

An industry insider has suggested Noah is making around £400 per video on TikTok, while Venezuela is likely to make £2,000 due to her following count of 1.3 million

In one video on their honeymoon, Noah asked his followers if they'd give them some more gifts now that they were married.

In a TikTok live viewed by 20,000 he said: 'Keep liking our videos people, keep sending gifts.'

After saying thank you to several of his followers he joked they should stick around on the livestream and 'watch Venezuela punch me in the mouth'.

The other half of the honeymooning couple said: 'I am, honestly!'

Noah previously confirmed that the pair don't share their finances after they were asked whether they have a shared bank account.

'She earns her money, I earn mine,' said Noah, as Venezuela joked: 'Yeah, what you gonna do about it.'

Noah went on to debunk the rumour that Tyson gave him £5million when he tied the knot with his daughter as he insisted: 'No Tyson did not give me £5million'.

Meanwhile Venezuela is being eyed up by executives for a fly on the wall TV series.

Noah went on to debunk the rumour that Tyson gave him £5million when he tied the knot with his daughter as he insisted: 'No Tyson did not give me £5million'

Boasting 1.3 million TikTok followers, Venezuela is already entertaining fans with her honest musings and candid moments, from cooking to kitting out her and Noah's static caravan home.

And following the success of the Netflix series At Home With The Furys, it is no wonder bosses are wanting to draw on the Fury popularity.

A TV insider said: 'The couple are not A-list celebrities but everyone has become obsessed with their love story.

'People are genuinely intrigued by them. Whether it’s the fact they have married so young, Venezuela’s famous family or their gypsy lifestyle, they have the ‘X factor'.

'Several TV executives think a proper fly-on-the-wall series following their lives as newlyweds in the gypsy community would be fascinating,' they told The Sun.

It is thought Netflix would be likely to produce the series due to their already established relationship with the Furys.

Venezuela's representatives told The Daily Mail: 'We have many offers on the table regarding Venezuela which we are discussing.'